As the Income Tax Return (ITR) filing season begins, one of the most common questions taxpayers ask is: How much income is tax-free? Is it ₹2.5 lakh, ₹5 lakh, ₹7 lakh, or ₹12 lakh? The answer depends on the type of income you earn and the tax regime you choose.

In this comprehensive guide, we will explain the tax-free income limits, rebate provisions, ITR filing thresholds, and the differences between the Old and New Tax Regimes for Financial Year (FY) 2025-26 (Assessment Year 2026-27).

Types of Income Under the Income Tax Act

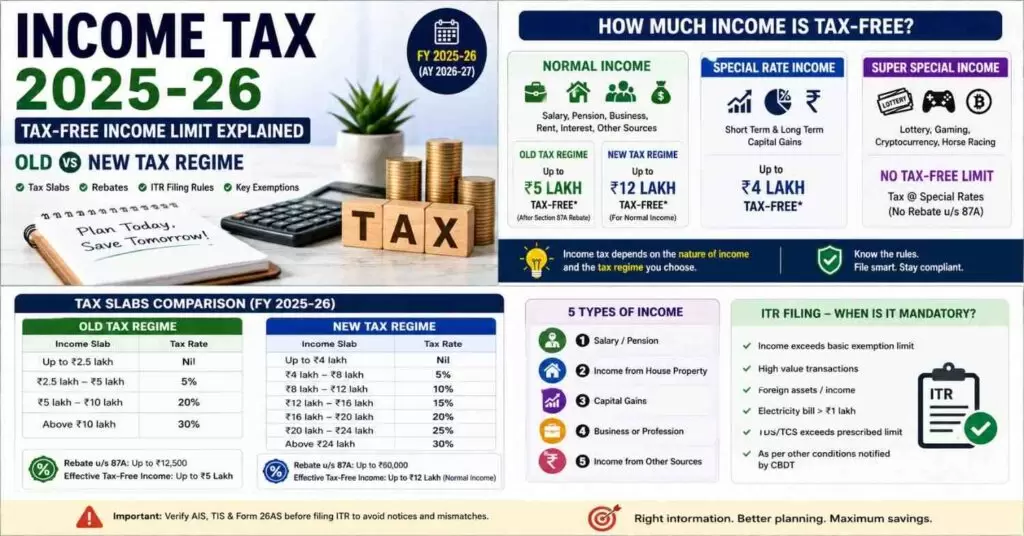

A taxpayer can earn income from five major sources:

1. Salary Income

This includes salary, wages, pension, bonuses, and other employment-related earnings.

2. Income from House Property

Rental income received from residential or commercial properties falls under this category.

3. Capital Gains

Income arising from the sale of shares, mutual funds, real estate, or other capital assets.

4. Business or Professional Income

Income earned through business activities, freelancing, professional services, trading, manufacturing, and related activities.

5. Income from Other Sources

Interest from savings accounts, fixed deposits, dividends, gifts, and miscellaneous earnings are included here.

Understanding the Nature of Income

Not all income is taxed in the same way. Broadly, income can be classified into three categories:

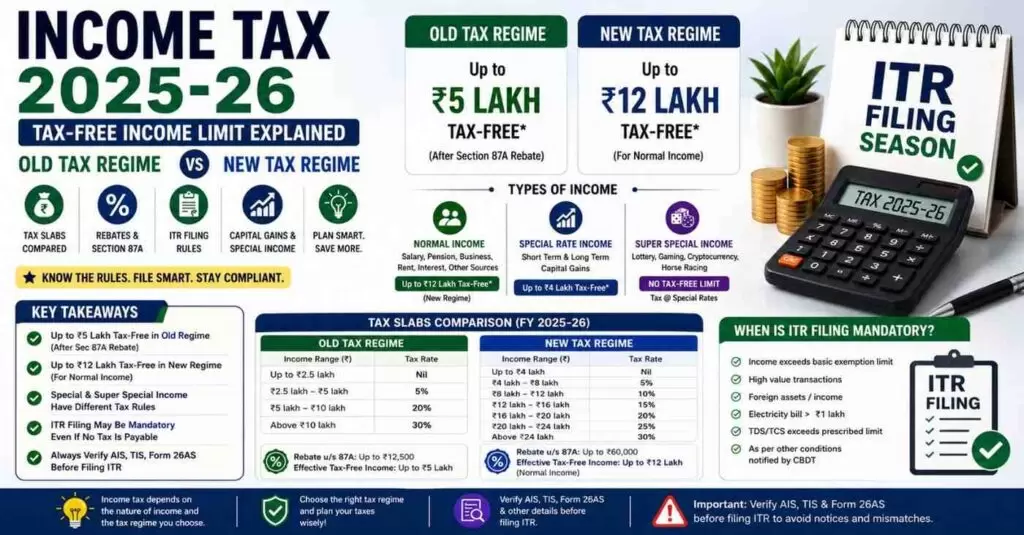

Normal Income

Income taxed according to slab rates under either the Old or New Tax Regime.

Special Rate Income

Typically includes short-term and long-term capital gains, which are taxed at specific rates prescribed by law.

Super Special Income

Income from lottery winnings, online gaming, cryptocurrency transactions, and horse racing. These incomes generally do not enjoy standard tax exemptions or rebates and are taxed at special rates.

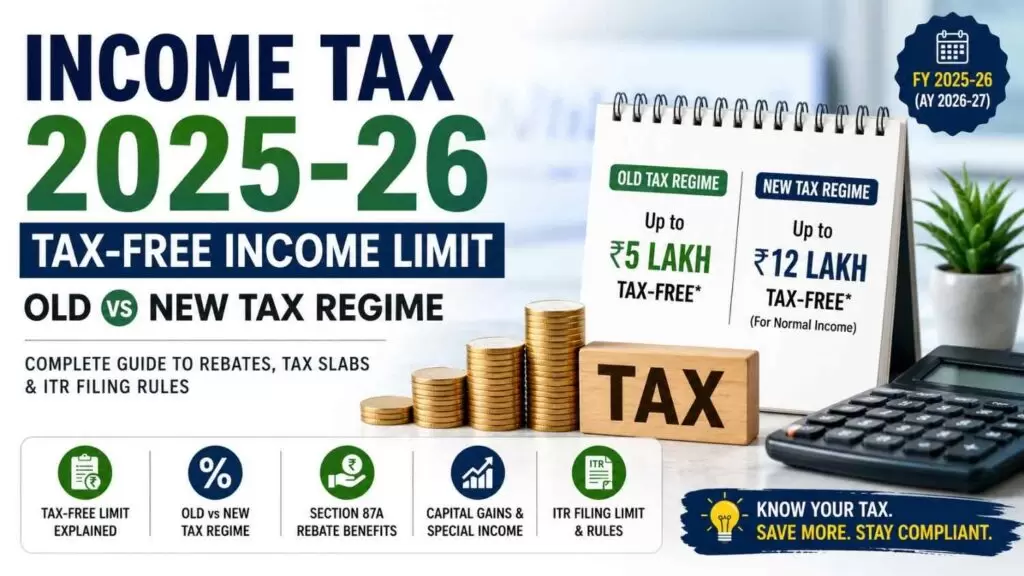

Old Tax Regime: Tax-Free Limit and Rebate

Under the Old Tax Regime, the basic tax structure remains:

- Up to ₹2.5 lakh: Nil tax

- ₹2.5 lakh to ₹5 lakh: 5%

- ₹5 lakh to ₹10 lakh: 20%

- Above ₹10 lakh: 30%

Section 87A Rebate

If your total taxable income does not exceed ₹5 lakh, you can claim a rebate under Section 87A of up to ₹12,500.

This effectively means:

- Income up to ₹5 lakh results in zero tax liability.

- Once income exceeds ₹5 lakh, the rebate is no longer available.

Therefore, for many individual taxpayers under the Old Tax Regime, the effective tax-free income limit is ₹5 lakh.

New Tax Regime: Tax-Free Income up to ₹12 Lakh

The New Tax Regime offers a different structure with lower tax rates and fewer deductions.

The revised slab rates are:

- Up to ₹4 lakh: Nil tax

- ₹4 lakh to ₹8 lakh: 5%

- ₹8 lakh to ₹12 lakh: 10%

- Higher slabs apply progressively beyond this level

Rebate Under the New Regime

A significant benefit of the New Tax Regime is the enhanced rebate mechanism.

For normal income:

- Tax liability up to ₹60,000 can be rebated.

- This effectively makes normal taxable income up to ₹12 lakh tax-free.

However, taxpayers must understand that this benefit primarily applies to normal income categories and not necessarily to special-rate incomes such as capital gains or lottery winnings.

Treatment of Capital Gains

Capital gains receive separate treatment under tax laws.

Long-Term Capital Gains (LTCG)

Long-term capital gains are taxed at special rates and generally do not qualify for the standard rebate available on normal income.

Short-Term Capital Gains (STCG)

Short-term capital gains also attract special tax rates depending on the nature of the asset and applicable provisions.

Therefore, even if your normal income qualifies for rebates, capital gains may still attract tax liability.

Taxation of Lottery, Gaming, and Cryptocurrency Income

Income earned from:

- Lottery winnings

- Online gaming

- Cryptocurrency transactions

- Horse racing

falls under special taxation rules.

Key points:

- No standard tax-free limit applies.

- No major rebate benefits are generally available.

- Such income may be taxed at a flat rate of 30% plus applicable surcharge and cess.

This is one of the most important areas where taxpayers often misunderstand tax exemptions.

ITR Filing Limits: When Is Filing Mandatory?

Many taxpayers confuse tax-free income with the requirement to file an ITR. These are not the same.

Under the Old Tax Regime

ITR filing generally becomes relevant once total income exceeds the basic exemption limit of ₹2.5 lakh.

Under the New Tax Regime

The practical threshold often discussed is ₹4 lakh, although filing requirements can vary depending on income type, transactions, and other prescribed conditions.

Even if no tax is payable due to rebates, filing an ITR may still be beneficial or mandatory in certain situations.

Tax-Free Income vs. Taxable Income

It is important to understand the distinction:

Tax-Free Income

Income on which no tax ultimately becomes payable due to exemptions or rebates.

Taxable Income

Income that falls within the tax framework and may attract tax depending on slabs, rebates, and deductions.

For example:

- A person earning ₹5 lakh under the Old Regime may calculate tax but eventually pay zero due to Section 87A.

- A person earning ₹12 lakh under the New Regime may similarly pay no tax because of the available rebate structure.

Choosing Between Old and New Tax Regimes

The right tax regime depends on your financial profile.

Old Tax Regime May Be Better If:

- You claim significant deductions.

- You invest heavily in tax-saving instruments.

- You pay home loan interest.

- You claim HRA and other exemptions.

New Tax Regime May Be Better If:

- You prefer simplicity.

- You have limited deductions.

- Your income mainly consists of salary or standard earnings.

- You want to benefit from the higher effective tax-free threshold.

Important Documents to Verify Before Filing ITR

Before submitting your return, always verify:

- AIS (Annual Information Statement)

- TIS (Taxpayer Information Summary)

- Form 26AS

- Salary documents and Form 16

- Bank interest certificates

- Capital gain statements

Cross-checking these records can help avoid notices, mismatches, and future complications.

Frequently Asked Questions (FAQs)

The tax-free income limit depends on the tax regime chosen. Under the Old Tax Regime, income up to ₹5 lakh can be tax-free after claiming the Section 87A rebate. Under the New Tax Regime, normal income up to ₹12 lakh may effectively attract zero tax due to the enhanced rebate provisions.

Yes, for most taxpayers earning normal income, such as salary, pension, business income, rental income, or interest income, tax liability can be zero up to ₹12 lakh due to the rebate available under the New Tax Regime. However, special-rate income, such as capital gains and lottery winnings, is treated differently.

Section 87A is a tax rebate available to eligible resident individuals. It reduces the tax liability of taxpayers whose income falls within the prescribed limits, helping many individuals pay little or no income tax.

No. Long-Term Capital Gains (LTCG) and Short-Term Capital Gains (STCG) are generally taxed at special rates and may not qualify for the same rebate benefits available on normal income under the New Tax Regime.

The best option depends on your financial situation. The Old Tax Regime may be beneficial if you claim multiple deductions and exemptions, while the New Tax Regime may suit taxpayers who prefer lower tax rates and a simpler tax structure with fewer deductions.

Final Thoughts

The biggest takeaway for FY 2025-26 is that tax liability depends not only on how much you earn but also on the type of income and the tax regime you choose.

In general:

- Under the Old Tax Regime, income up to ₹5 lakh can effectively be tax-free due to the Section 87A rebate.

- Under the New Tax Regime, normal income up to ₹12 lakh may attract zero tax because of the enhanced rebate provisions.

- Capital gains, cryptocurrency income, lottery winnings, and gaming income follow different taxation rules and may not enjoy these benefits.

Tax laws can be complex, and every taxpayer’s situation is unique. When in doubt, consult a qualified tax professional and review all tax records carefully before filing your return.

A well-prepared return not only ensures compliance but also helps you make the most of the benefits available under the Income Tax Act.

Thank you for reading this post, don't forget to subscribe!