Tax loss harvesting is a legitimate, IRS‑sanctioned tax strategy that lets investors use realized investment losses to reduce taxable gains — and in some cases ordinary income. When done correctly, it can improve after‑tax returns without changing your long‑term investment plan. (Encyclopedia Britannica)

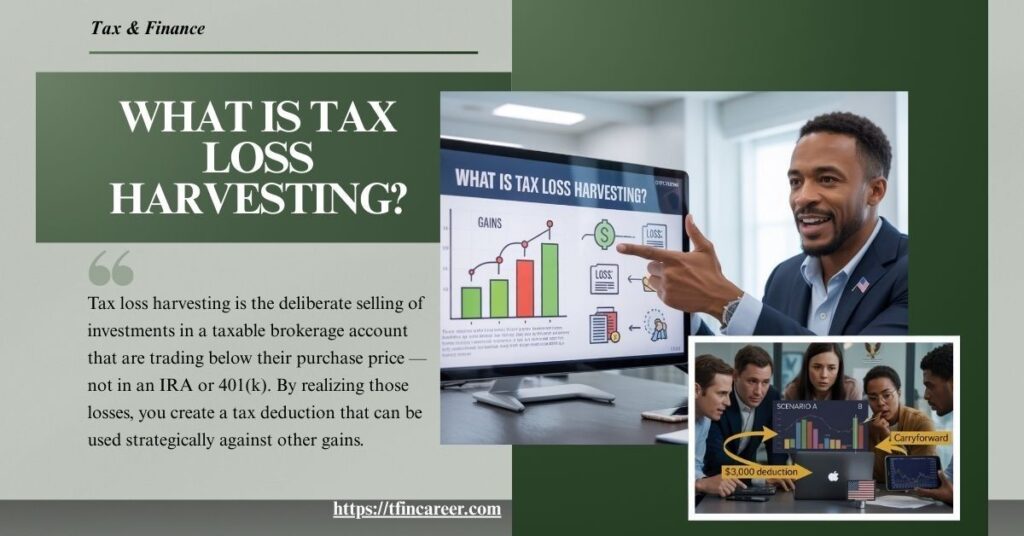

What Is Tax Loss Harvesting?

Tax loss harvesting is the deliberate selling of investments in a taxable brokerage account that are trading below their purchase price — not in an IRA or 401(k). By realizing those losses, you create a tax deduction that can be used strategically against other gains. (Encyclopedia Britannica)

At its core, the idea is simple:

- Realized gains (from sales of investments that made money) are taxable.

- Realized losses (from sales of investments that lost money) can offset those gains.

- Any net loss beyond gains can reduce ordinary income up to $3,000 per year, with the rest carried forward indefinitely. (Encyclopedia Britannica)

Read this Article Before Filing you Tax Return: 2025 Tax Changes You Need to Know Before Filing

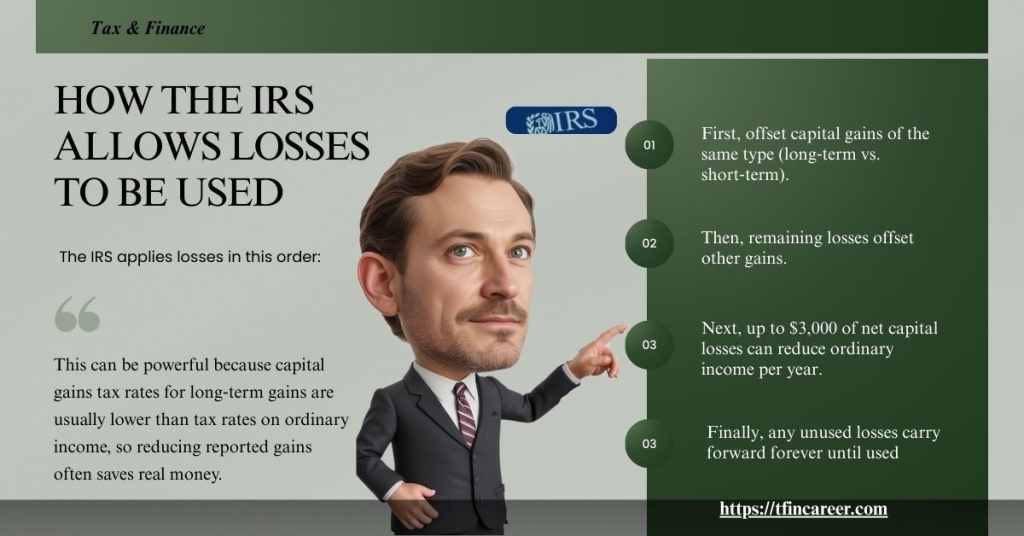

How the IRS Allows Losses to Be Used

The IRS applies losses in this order:

- First, offset capital gains of the same type (long‑term vs. short‑term).

- Then, remaining losses offset other gains.

- Next, up to $3,000 of net capital losses can reduce ordinary income per year.

- Finally, any unused losses carry forward forever until used. (Encyclopedia Britannica)

This can be powerful because capital gains tax rates for long‑term gains are usually lower than tax rates on ordinary income, so reducing reported gains often saves real money.

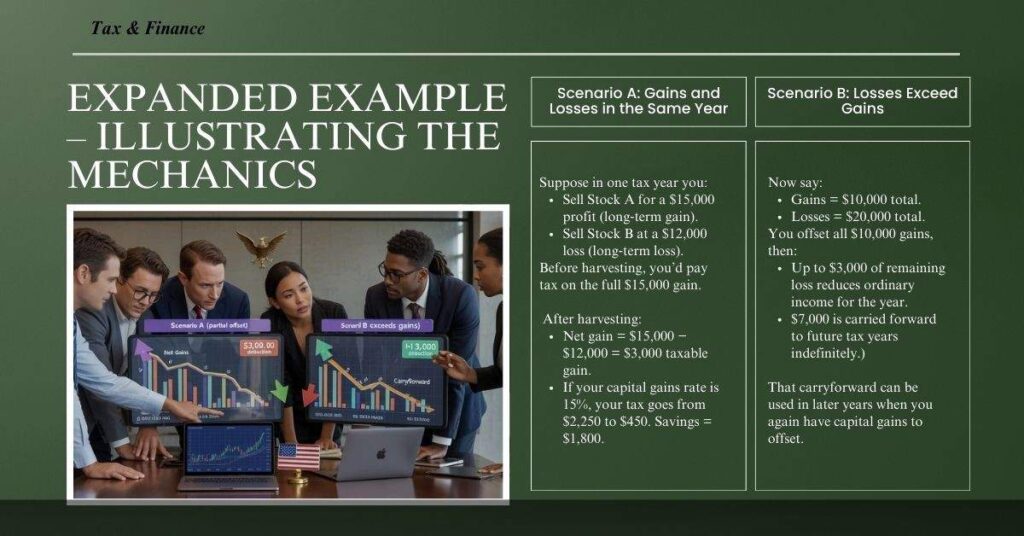

Expanded Example – Illustrating the Mechanics

Scenario A: Gains and Losses in the Same Year

Suppose in one tax year you:

- Sell Stock A for a $15,000 profit (long‑term gain).

- Sell Stock B at a $12,000 loss (long‑term loss).

Before harvesting, you’d pay tax on the full $15,000 gain. After harvesting:

- Net gain = $15,000 − $12,000 = $3,000 taxable gain.

- If your capital gains rate is 15%, your tax goes from $2,250 to $450. Savings = $1,800. (Encyclopedia Britannica)

Scenario B: Losses Exceed Gains

Now say:

- Gains = $10,000 total.

- Losses = $20,000 total.

You offset all $10,000 gains, then:

- Up to $3,000 of remaining loss reduces ordinary income for the year.

- $7,000 is carried forward to future tax years indefinitely. (Encyclopedia Britannica)

That carryforward can be used in later years when you again have capital gains to offset.

How to Pay Less Tax on Investments in 2025 Using IRS Capital Gains Tax Worksheet

The IRS Wash Sale Rule (Very Important!)

A key limitation is the IRS’s wash sale rule. Under U.S. tax law:

- If you sell a security at a loss and then repurchase the same or “substantially identical” security within 30 days before or after the sale,

- The IRS disallows the loss for tax purposes. (Wikipedia)

This rule is meant to prevent taxpayers from selling and buying essentially the same investment solely to create artificial losses.

Example of a wash sale:

If you sell 100 shares of XYZ at a loss, then buy those same shares back 10 days later, the IRS won’t let you use that loss to offset gains. It must be outside the 30‑day window. (Wikipedia)

A subtle point: losses disallowed by wash sales are not gone forever — they are typically added to the cost basis of the repurchased shares, affecting the eventual gain/loss when those are sold later. (Kiplinger)

Strategic Considerations for Investors

1. Timing Matters

To count for a given tax year, you must realize the loss before year‑end (e.g., by Dec. 31, 2025). The IRS uses the trade date for this purpose. Waiting until the last minute can complicate wash sale timing and record‑keeping.

2. Type of Gains and Losses

Capital gains and losses have categories:

- Short‑term: held ≤ 1 year (taxed at ordinary income rates).

- Long‑term: held > 1 year (taxed at lower preferential rates). (Encyclopedia Britannica)

Match losses to the same category of gains where possible before applying them more broadly.

3. Portfolio Management

Tax loss harvesting is most effective when:

- You have a mix of winners and losers.

- You’re rebalancing or pruning underperformers.

It also forces you to evaluate whether an underperforming asset still fits your long‑term plan rather than mindlessly holding it.

When Tax Loss Harvesting Makes Sense

This strategy is most valuable when:

- You have large realized gains in a taxable account.

- You are already planning portfolio rebalancing.

- Want to lower tax drag on long‑term compounding.

- You are in a higher tax bracket — deferring or reducing taxes now can improve lifetime after‑tax returns.

It’s less relevant if you only have unrealized losses (losses on positions you haven’t sold), because losses must be realized to matter for tax purposes. (Encyclopedia Britannica)

Pros of Tax Loss Harvesting

| ADVANTAGE | WHY IT MATTERS |

| Lowers Your Tax Bill | Losses offset gains and may reduce taxes now. (Encyclopedia Britannica) |

| Boosts After‑Tax Returns | More money stays invested and grows over time. (Forbes) |

| Portfolio Rebalancing | Selling losers can help rebalance your holdings. (Encyclopedia Britannica) |

| Carry Forward Long‑Term | Unused losses can be used in future years. (NerdWallet) |

Cons of Tax Loss Harvesting

| DRAWBACK | WHAT TO WATCH OUT FOR |

| Wash Sale Rules Are Strict | If you repurchase too soon, losses may be disallowed. (Empower) |

| Can Affect Investment Strategy | Selling a loser just for taxes might hurt long‑term plans. (TheStreet) |

| Transaction Costs Add Up | More trades can mean more fees. (Forbes) |

| Complex Record‑Keeping | You must track lots of details for IRS reporting. (Forbes) |

Caveats and Professional Tips

Portfolio Consistency

Don’t let tax motives override sound investment strategy. Selling just for the tax benefit without regard to long‑term fit may harm total returns. Experts recommend harvesting selectively and with a plan.

Automation Tools

Many modern brokerages and robo‑advisors include automated tax‑loss harvesting that identifies opportunities and tracks wash sale windows — useful for complex portfolios or frequent traders. (Encyclopedia Britannica)

Record‑Keeping

To claim deductions and carry forward losses, you must report transactions accurately on IRS forms (e.g., Schedule D and Form 8949).

Summary: Steps to Implement Tax Loss Harvesting

- Review holdings periodically for unrealized losses.

- Sell loss‑making positions in taxable accounts — before year‑end.

- Offset gains first, then ordinary income (up to $3,000).

- Avoid wash sales by observing the 30‑day rule.

- Carry forward unused losses to future years.

- Reinvest thoughtfully to maintain risk and return objectives.

Tax loss harvesting isn’t a magic bullet, but it can be a powerful piece of tax‑efficient investing when used deliberately and in harmony with your financial plan. Consulting a tax professional or financial advisor can help tailor it to your situation and ensure compliance with IRS rules. (Encyclopedia Britannica)

Hi there! I am Sudip Sengupta, the face behind “Tfin Career”. Tfin Career is a sole proprietorship finance and consulting firm that makes complex tax and financial concepts easy to understand for everyone. With more than 21 years of experience in the field, I have noticed that people cannot make the right decisions in this field. So, I decided to create “Tfin Career” to help individuals and businesses alike. Here I urge those who are confused to make better choices. Also, it is good news for my dear clients and every visitor that I/we are going to start a training module for those who want to choose a career path in Finance and Taxation. Just follow my website.

Thank you for reading this post, don't forget to subscribe!