Imagine selling a $1M+ asset and walking away without owing the IRS a dime on federal capital gains tax. Sounds like a fairy tale? It’s not. Every year, investors, founders, and ordinary taxpayers use smart, legal IRS strategies to reduce — or even eliminate — capital gains tax. This guide (updated for 2026 rules) breaks down the best ways to do it in plain English, with clear examples you can actually follow.

Important: These are legal planning strategies, not evasion or loopholes. Always check with a CPA or tax pro before acting.

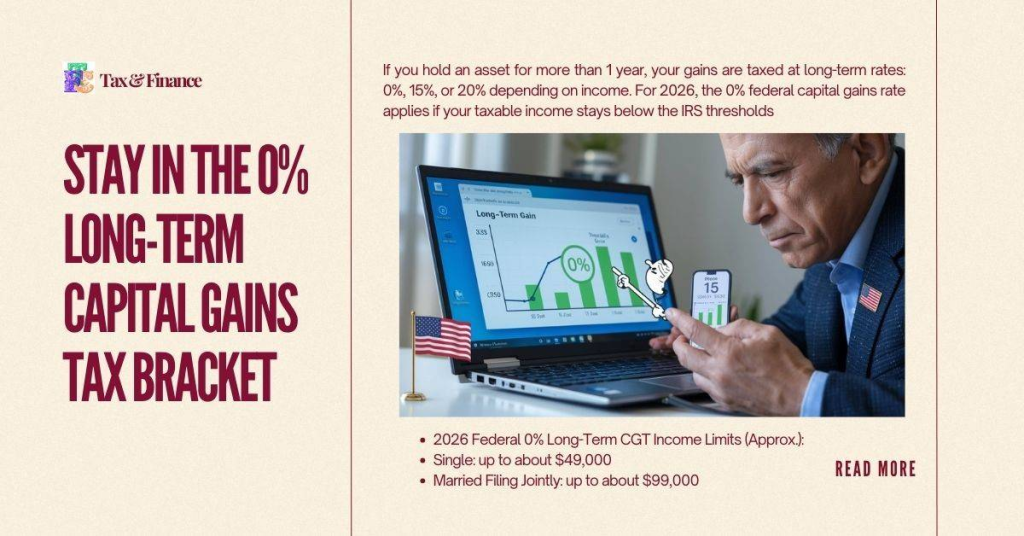

1) Stay in the 0% Long-Term Capital Gains Tax Bracket

If you hold an asset for more than 1 year, your gains are taxed at long-term rates: 0%, 15%, or 20% depending on income. For 2026, the 0% federal capital gains rate applies if your taxable income stays below the IRS thresholds. (Kiplinger)

- 2026 Federal 0% Long-Term CGT Income Limits (Approx.):

- Single: up to about $49,000

- Married Filing Jointly: up to about $99,000 (Kiplinger)

Example on Capital Gains Tax

You sell long-held stock for $1,000,000 but after deductions your total taxable income is $90,000 as a couple. Since that’s under the 0% bracket, your federal tax on the gain may be 0%.

Claculate Your’s Capital Gains Tax 2025-2026: Estimate Your IRS Liability – Free Tool

Pros

- Simple — no special structures

- Works for most long-term assets

Cons

- Income must be low enough

- State taxes may still apply

- Small changes in income can push you into 15% or higher brackets

Read this Related Article: How It’s Possible to Legally Pay Zero Federal Income Tax

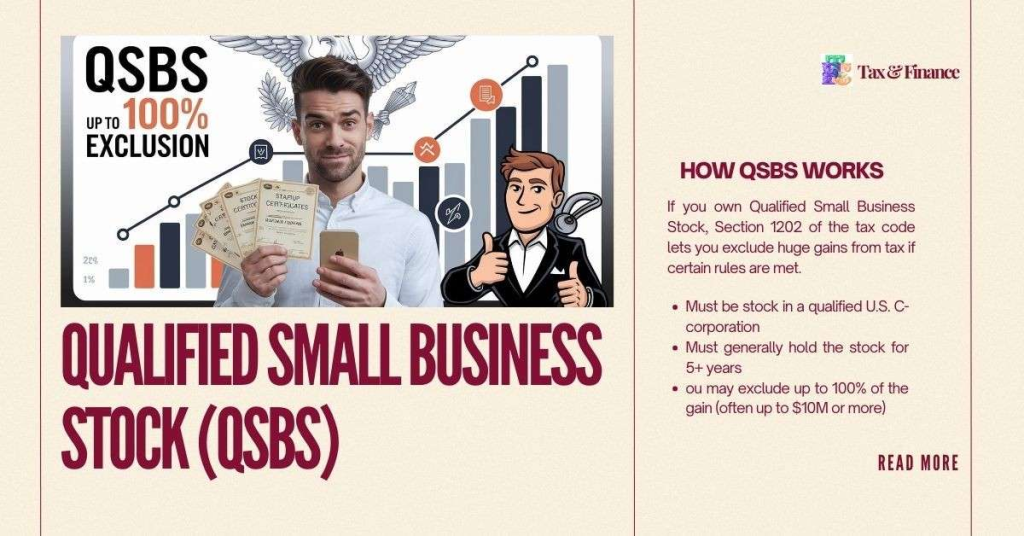

2) Qualified Small Business Stock (QSBS) — Big for Founders & Angels

If you own Qualified Small Business Stock, Section 1202 of the tax code lets you exclude huge gains from tax if certain rules are met. (Bequests and Online Legacy Planning)

How QSBS Works

- Must be stock in a qualified U.S. C-corporation

- Must generally hold the stock for 5+ years

- ou may exclude up to 100% of the gain (often up to $10M or more) (Bequests and Online Legacy Planning)

Example on Capital Gains Tax

Dan buys QSBS in a startup for $1 million. Five years later he sells it for $16 million. If the rules apply, Dan excludes the first $15M of gain from federal tax.

Pros

- Massive federal tax exclusion

- Especially great for founders & early investors

Cons

- Complex qualification rules

- Must meet holding period & business tests

3) Sell Your Home? Use the Primary Residence Exclusion

If you sell your main home, the IRS lets you skip federal tax on a huge chunk of the gain. Under Section 121:

- $250,000 excluded for single filers

- $500,000 excluded for joint filers

You must have lived in the home 2 of the last 5 years to qualify. (Business Insider)

Example on Capital Gains Tax

Jamie and Alex sell their long-time family home and make $450,000 in gain. Because they meet the residency test, they pay $0 federal tax on the gain.

Pros

- Very generous tax cut for real home sellers

- Rules are easy to understand

Cons

- Only applies to your primary home

- Must meet ownership + use tests

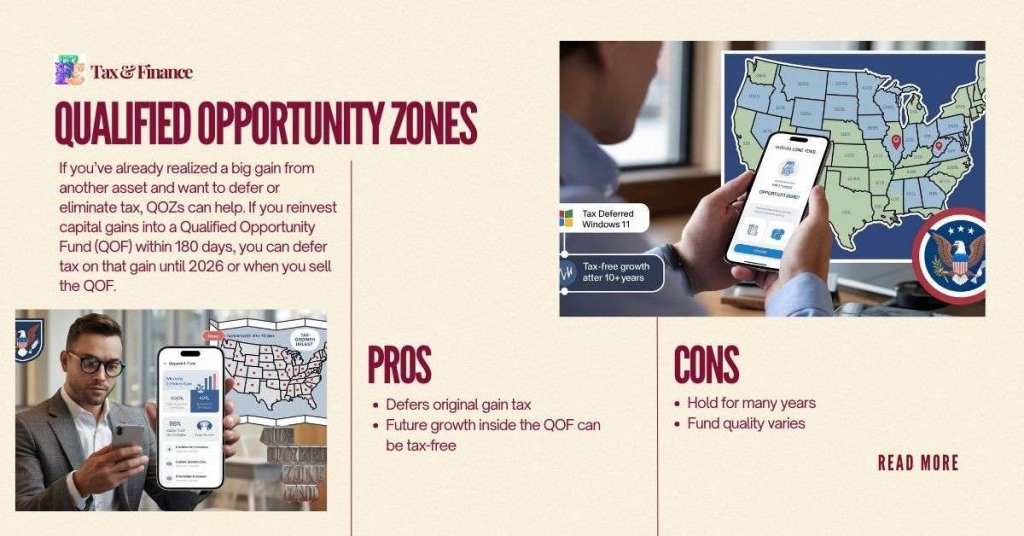

4) Qualified Opportunity Zones (QOZ)

If you’ve already realized a big gain from another asset and want to defer or eliminate tax, QOZs can help. If you reinvest capital gains into a Qualified Opportunity Fund (QOF) within 180 days, you can defer tax on that gain until 2026 or when you sell the QOF. (LegalClarity)

Plus, if you hold the QOF investment for 10+ years, gains on the QOF investment are tax-free.

Pros

- Defers original gain tax

- Future growth inside the QOF can be tax-free

Cons

- Hold for many years

- Fund quality varies

5) Installment Sales — Spread the Tax Bite

Instead of recognizing all the gain in one year, you can sell an asset and receive payments over time. This spreads the gain (and tax) over multiple years. (LegalClarity)

Pros

- Can reduce taxable income in high tax years

- Keeps you potentially in lower brackets

Cons

- You don’t get all your cash up front

- Must report properly on IRS Form 6252

6) Use Tax-Advantaged Accounts (Roth, HSA, 529)

Certain accounts legally shelter gains forever:

- Roth IRA / Roth 401(k): Buy/sell inside the account without capital gains tax, and qualified withdrawals are tax-free. (LegalClarity)

- Health Savings Account (HSA): Triple tax benefits — gains are tax-free if used for medical costs. (LegalClarity)

- 529 College Savings Plan: Gains are tax-free when used for qualified education. (LegalClarity)

Pros

- True tax-free gains

- Great for long-term planning

Cons

- Must meet specific qualified use rules

- Roth conversion may trigger ordinary income tax

7) Harvest Losses & Offset Gains

If some of your investments have dropped in value, selling them to realize a capital loss can offset gains elsewhere — reducing or eliminating taxable gains. (Sloan Advisory Group)

Pros

- Reduces taxable gains dollar-for-dollar

- Can carry losses forward

Cons

- Must follow wash sale rules

- Doesn’t erase tax on all gains if losses are limited

8) Donate Appreciated Assets to Charity

Instead of selling an appreciated stock or property, donating it directly to a qualified charity can avoid capital gains tax entirely, and you may get a deduction. (Enrichest)

Pros

- Eliminates capital gains tax

- Supports a cause

Cons

- Must itemize deductions

- The charity needs to be able to accept the assets

9) Manage Your Income & Timing

Sometimes when you sell matters just as much as what you sell. If you sell in a year when your income is low — for example, after retirement — you may stay in the 0% bracket or a lower rate. (NerdWallet)

Pros

No special structures needed

Cons

- Requires good planning

- Timing life events isn’t always predictable

Your user Frendly Tax Software – TurboTax Free Edition Explained 2026: Everything You Need To Know

Quick Checklist on Capital Gains Tax Before You Sell

- Check if your gain can fit in the 0% federal bracket

- Could your asset qualify for QSBS?

- Did you live in your home long enough for the residence exclusion?

- Can you defer tax with a QOZ investment?

- Could an installment sale help?

- Can you offset with losses or donate instead of selling?

Capital Gains Tax FAQ — Clear Answers for Real Planning

1. What makes long-term Capital Gains Tax 0% federally?

If your taxable income (after deductions) falls under the IRS 0% long-term capital gains bracket, your federal tax on gains can be $0. For 2026, that threshold is roughly:

• Single: ~$49,450

• Married filing jointly: ~$98,900 (Kiplinger)

Note: This rate applies only to long-term Capital Gains Tax (assets held > 1 year). Short-term gains are taxed at ordinary income rates.

2. Do long-term gains count toward income for the 0% bracket?

Yes. Long-term gains are included in taxable income for determining the bracket. So if your ordinary income is low enough, you might still fit under the 0% rate even with large long-term gains. (Kiplinger)

3. Can I time my sale to qualify for 0%?

Yes, timing matters. Selling in a year when your ordinary income is low — for example after retiring or taking a sabbatical — may help you land in the 0% bracket. (Gov Capital)

4. What’s QSBS and how can it eliminate tax?

Qualified Small Business Stock (QSBS) under IRS Section 1202 can let you exclude up to 100% of gain if:

• The stock is from a qualified U.S. C-corporation, and

• You hold it for the required period (generally 5+ years). (LegalClarity)

Recent changes (post-2025):

- 50% exclusion after 3 years

- Your next exclusion After 4 years 75%

- 100% after 5 years

This means even partial exclusion can significantly cut taxes. (Greenberg Traurig)

5. What is an Opportunity Zone and can it eliminate tax?

Qualified Opportunity Zones (QOZs) let you defer gains by reinvesting them into a Qualified Opportunity Fund (QOF) within 180 days of sale.

• Original gain tax is deferred until sale or Dec 31, 2026.

• After holding the QOF investment for 10+ years, future appreciation can be entirely tax-free. (LegalClarity)

6. Do state capital gains tax matter?

Yes. Even if you pay $0 federal tax, many states tax capital gains as ordinary income — though some states like Texas, Florida, and Missouri don’t tax gains at all on the state level. (Investopedia)

7. What’s tax-loss harvesting and does it help?

Tax-loss harvesting means selling investments at a loss to offset gains elsewhere, reducing taxable gains dollar-for-dollar. You can also carry forward unused losses to future years. Just be careful of the wash-sale rule (don’t rebuy the same asset within 30 days). (MoneyPulses)

8. How does selling my home work with capital gains?

If you sell your primary residence, the IRS lets you exclude up to:

• $250,000 gain (single)

• $500,000 gain (married filing jointly)

You must have lived there 2 of the last 5 years. This is separate from investment gains. (KPMG)

9. What are installment sales and how do they help?

An installment sale lets you spread the recognition of gain over several years, potentially keeping you in a lower bracket and reducing taxes in high-income years. You report gains as you receive payments. (LegalClarity)

10. Do tax-advantaged accounts eliminate capital gains tax?

Yes — within specific accounts:

• Roth IRA / Roth 401(k): Buy and sell without taxes; qualified withdrawals are tax-free.

• HSA / 529 Plans: Gains are tax-free if used for qualified expenses. (MoneyPulses)

Conclusion — Smart Planning Beats Wishful Thinking

Paying zero federal capital gains tax on huge profits isn’t magic — it’s planning. Whether it’s timing your sale, using powerful IRS tax codes like QSBS or Opportunity Zones, or sheltering gains in a Roth or HSA, there are real tools available today.

Pro Tip: Combine strategies — for example, use tax-loss harvesting and timing to stay in the 0% bracket before a big sale.

Claculate Your’s Capital Gains Tax 2025-2026: Estimate Your IRS Liability – Free Tool

Disclaimer: This guide is educational. Tax law changes, and your situation is unique. Always consult a CPA or tax advisor before major financial moves.

Thank you for reading this post, don't forget to subscribe!