2025 New Savings Opportunities:The2025 tax year (filed in 2026)presents new opportunities for middle-income earners to reduce their tax burden. Below, we break down four key strategies to maximize savings, providing clear explanations, actionable tips, and an explanation of why each method matters.

1. Leverage Retirement Contributions

New Savings Opportunities: Why It Matters:

Contributing totax-advantaged retirement accountsreduces yourtaxable income, meaning you pay less in taxes now while growing savings for the future.

Key Accounts & Limits (2025):

- 401(k) / 403(b) / TSP:**23,500∗∗max contribution (up from 23,500∗∗max contribution (up from 23,000 in 2024).

- IRA (Traditional or Roth):**7,000∗∗(7,000∗∗(8,000 if age 50+).

- SEP IRA / Solo 401(k):For self-employed, up to25% of net earningsor$69,000(whichever is lower).

Pro Tips:

✔Traditional 401(k)/IRA = Tax Deduction Now

- Lowers your2025 taxable income(e.g., contributing 10,000 could save you∗∗10,000could save you∗∗2,200** if in the 22% bracket).

✔Roth 401(k)/IRA = Tax-Free Withdrawals Later - It’s better to expecthigher taxes in retirement.

✔Employer Match = Free Money - Always contribute enough to receive the full match (e.g., if your employer matches 5%, contribute at least 5% as well).

Who Benefits Most from New Savings Opportunities?

- Middle-income earners nearbracket thresholds(e.g., $104,250 for single filers in the 22% bracket).

- Self-employed individuals cansupercharge retirement savingswith a SEP IRA.

Also read, Top 5 Tax Breaks for 50+: Take Full Benefits Of Tax-Saving Opportunities

2. Use HSAs & FSAs (Tax-Free Healthcare Savings)

Why It Matters:

- HSAs (Health Savings Accounts):Triple tax benefit(deductible contributions, tax-free growth, tax-free withdrawals for medical expenses).

- FSAs (Flexible Spending Accounts):Use-it-or-lose-it funds for medical and dependent care, reducing taxable income.

New Savings Opportunities: Contribution Limits

- HSA:

- 4,300∗∗(individual)/∗∗4,300∗∗(individual)/∗∗8,600(family).

- +$1,000 catch-upif age 55+.

- FSA:

- $3,200(healthcare FSA).

- $5,000(dependent care FSA).

Pro Tips:

✔Max Out HSA First(If Eligible)

- Requires ahigh-deductible health plan (HDHP).

- Can invest HSA funds for long-term growth (like a retirement account).

✔FSA: Plan Carefully - Estimate medical expenses (e.g., prescriptions, glasses) to avoid forfeiting unused funds.

✔“Double Benefit” Strategy - Pay medical bills withHSA funds now, but save receipts and reimburse yourselfyears laterfor tax-free cash.

Who Benefits Most from New Savings Opportunities?

- Families withhigh medical costs.

- Healthy individuals who caninvest HSA fundsfor future tax-free withdrawals.

Know more about Claiming Tax Deductions for Significant Healthcare Costs

3. Strategic Deductions (Lower Taxable Income Further)

Why It Matters:

Thestandard deductionis higher in 2025 (15,100 single/15,100 single/30,200 married), butitemizing deductionscan save more if you have:

- Largecharitable donations

- Highmortgage interest/property taxes

- Significantmedical expenses(above 7.5% of AGI)

Key Strategies New Savings Opportunities:

✔“Bunching” Charitable Donations

- Instead of giving 5,000 yearly, give∗∗5,000 yearly, give∗∗10,000 every other year** to exceed the standard deduction and itemize.

✔Tax-Loss Harvesting (For Investors) - Sell losing stocks tooffset capital gains(e.g., if you have $3,000 in losses, you can deduct them against ordinary income).

✔Medical Expense Deduction - Only counts if it exceeds 7.5% of AGI (e.g., if AGI is 100,000, only expenses over∗∗100,000, and only expenses over∗∗7,500** count).

Pro Tips:

- Donor-Advised Funds (DAFs):Contribute a lump sum, get an immediate deduction, and distribute funds to charities over time.

- Prepay State Taxes (If Itemizing):Pay2026 state taxes in December 2025to claim the deduction early.

Who Benefits Most from New Savings Opportunities?

- Homeowners withmortgage interest & property taxes.

- Investors withcapital gains to offset.

Charitable Contributions for Tax Deduction: Donating Goods is Just as Valuable as Cash

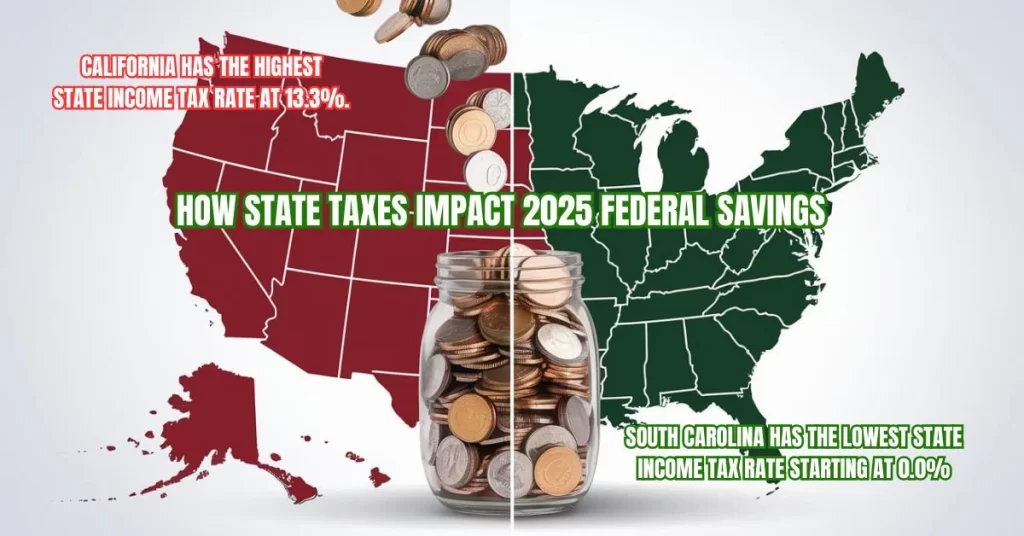

4. Check State Tax Implications

Why It Matters:

Federal tax savings can beoffset by state taxesin high-tax states, such as California and New York. Meanwhile, no-income-tax states, such as Texas and Florida, let you keep more.

Key Considerations New Savings Opportunities:

✔State Tax Deductions on Federal Returns

- If you pay **10,000 in state taxes∗∗, you can deduct them∗∗if itemizing∗∗(capped at 10,000 in state taxes∗∗, you can deduct them∗∗if itemizing∗∗(capped at 10,000 under SALT).

✔Relocation for Tax Savings? - Moving fromCalifornia (13.3% top rate) to Texas (0%)could result in significant savings.

✔Tax Credits for Middle-Income Earners - Some states offerproperty tax relieforchild tax credits.

Pro Tips:

- Work Remotely?Some states tax remote workers—check residency rules.

- Municipal Bonds:Tax-free interest in your state (e.g., NY muni bonds are exempt from NY & federal taxes).

Who Benefits Most?

- High earners inhigh-tax states.

- Remote workers who canrelocate to tax-friendly states.

5 Most Googled Questions About 2025 taxes(filed in 2026), Based on IRS Updates and New Savings Opportunities, along with clear answers:

1. “What are the new tax brackets for 2025?”

Answer:

The IRS adjusted 2025 tax brackets for inflation. Key changes include:

- Single filers:

- 12% bracket:Up to **48,850 (from47,150 in 2024).

- 22% bracket:Up to **104,250 (from100,525).

- Married filing jointly:

- 12% bracket:Up to **97,700 (from94,300).

- 22% bracket:Up to **208,500 (from201,050).

2. “How much is the standard deduction in 2025?”

Answer:

- Single filers:**15,100∗∗(up15,100∗∗(up 400 from 2024).

- Married filing jointly:**30,200∗∗(up 30,200∗∗(up800).

- Head of household:**22,500∗∗(up 22,500∗∗(up600) .

3. “Will the Child Tax Credit increase in 2025?”

Answer:

Undercurrent law, the maximum Child Tax Credit remains **2,000 per child∗∗(2,000 per child∗∗(1,700 refundable). However, Congress may pass legislation to expand it later in 2025. The IRS will automatically adjust refunds if changes occur.

4. “When are 2025 taxes due?”

Answer:

- Deadline:April 15, 2026(for most taxpayers).

- Extensions:File byOctober 15, 2026, but taxes owed must still be paid by April 15 to avoid penalties.

5. “How can I reduce my 2025 taxable income?”

Answer:Top strategies include:

- Max out retirement accounts:Contribute23,500 to a 401(k)∗∗or∗∗23,500 to a 401(k)∗∗or∗∗7,000 to an IRA.

- Use HSAs:Contribute4,300(individual)∗∗or∗∗4,300(individual)∗∗or∗∗8,600 (family)for triple tax benefits.

- Itemize deductionsif they exceed the standard deduction (e.g., mortgage interest, charitable donations).

Bonus:For real-time updates, check theIRS websiteor consult a tax professional. Need more details? Ask about specific credits (e.g., EITC, Clean Vehicle Credit) or state tax changes!

Final Checklist for 2025 New Savings Opportunities

✅Max out 401(k)/IRA(Lower taxable income now).

✅Use HSA for medical + investments(Triple tax advantage).

✅Bunch deductions if near itemizing threshold.

✅Check state tax impact(Could save more by moving or optimizing).

Next Step:Use theIRS Withholding Calculatorto adjust paycheck withholdings and avoid a surprise bill in 2026.

For real-time updates, check theIRS websiteor consult a tax professional. Need more details? Ask about specific credits (e.g., EITC, Clean Vehicle Credit) or state tax changes!

Would you like acustomized tax planbased on your income and state? Let me know!